Examining the monthly “subscription” costs of a car.

I was scrolling through Twitter the other day when I came across the alarming little nugget that I’ve screenshotted above.

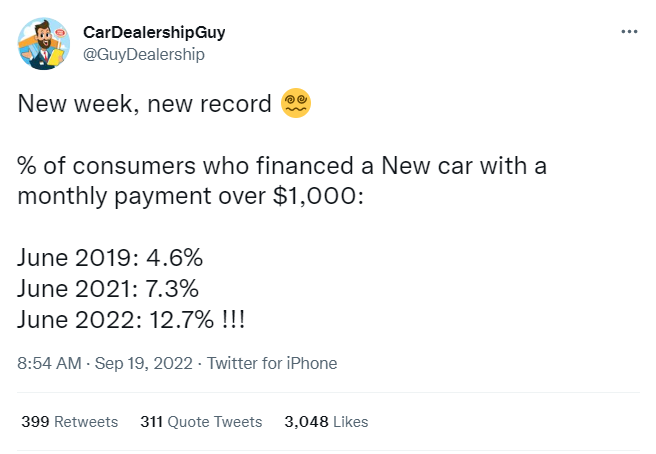

Those figures are pure insanity. Especially given that most people are not making anywhere near enough in income to justify buying a depreciating liability that costs $1,000+ a month. You make baller income or pay in cash, sure, okay. But when the average income in the U.S. is around $63,000, a monthly payment of $1,000 comes out to almost 20% of your annual income.

That’s ridiculously too much. Yet nearly an eighth of car-buying Americans are doing just that, according to the Tweet above.

Mind you, that $1,000 figure doesn’t include other ongoing vehicle expenses like gas, maintenance, or accessories. I mean, how can you live without a set of hand crafted custom crystallized wheels with genuine European crystals? I sure can’t.

And also mind you, that figure doesn’t include interest payments that can dramatically compound the costs of a vehicle over time. Especially if you miss a payment, or roll an auto loan over into another vehicle later on.

Bottom line: Americans pay WAY, WAY too much for blocks of metal, rubber, and plastic to get to work and the grocery store.

The tweet also got me thinking about how much I’ve spent on my own car. As I mentioned in an article here, I drive a “senior vehicle.” A 2006 Saturn that I purchased in 2011.

The retail cost of my car was $7,500, though I had to use sky-high interest rate financing at the time of purchase as my credit/income were not good. However, I managed to pay off the whole loan about two years later. Including interest and taxes, the total cost of “Baby” (my nickname for her) came to about $9,000.

I’ve owned Baby for going on twelve years now, as I bought her in January of 2011. That’s 141 months, including this month of September.

So, how much has it cost me overall to own a set of wheels?

It comes out to $63.80 a month.

That’s less than what I pay for my monthly Verizon smartphone bill (about $77 for unlimited data). That’s slightly more than what I pay for my electric bill on average ($50-$60). Its actually less than what I pay for gas in a typical month to feed my senior vehicle ($60-$70).

It’s also less than one tenth the cost of the average monthly car payment in the U.S. ($667).

Of course, I’ve excluded things like maintenance and fuel. I’m only factoring in the total retail cost of the vehicle itself, as the tweet above does for the financed vehicles.

Used cars, especially senior cars, often come with unexpected issues, in addition to the standard ongoing maintenance costs. I recently bought new tires for my car for about $600, for instance. I make sure she gets regular oil changes. And I’ve replaced brakes, and paid for other things as needed over our decade-long relationship. When I first bought her, I had to shell out over two thousand dollars for some electrical repairs and a new water pump. But for the vast majority of the time, she’s been remarkably reliable and cost-effective. Honestly, she could blow up right now, and she’d still have paid for herself many, many times over.

Often, new cars, and some newer used ones, will have warranties or maintenance offers from the dealership. These can make it appear that you’re “saving” money on repairs or maintenance. Except all of that is calculated into the retail price. So those “free” oil changes you’re getting, or the replacement part you need that’s “covered” by the warranty— yeah, you’re still paying for that, just maybe not directly as you would if you brought in a senior car like mine to a mechanic and paid out of pocket.

But even if you do actually save money on major repairs through a warranty, you still come out way ahead with a decent used car than a new one.

Granted, not many people are as loyal to their senior vehicles as I am. Not many people are willing to drive around in the same car for that long. Especially one that’s far from glamorous. Most people look to upgrade their cars the second they get a raise at work, or change into a better job. And to be fair, some people need newer vehicles for work, or because of where they live.

Sometimes it’s impossible to escape the money-sucking event horizon of the black hole that is car costs.

But that doesn’t mean you should purposefully set yourself up with an overpriced vehicle you don’t need that eats up your monthly budget. Do you really need to pay $37,876 just so you look cool when you go to the grocery store? That’s the average price of a new car, according to Financial Samurai.

Trust me, nobody cares what you drive. I can’t even remember the last time I saw a cool car on the road (like a Lambo, or higher-end Porsche), much less the person who drove it, because I deleted it from my memory bank so quickly.

I’ve been fortunate in that for a long time I’ve lived close to work, or driven company trucks, so I didn’t always need to 100% rely on my senior car as others do to get to work or get around town. But my car has done multiple road trips across the country, and survived ten North Dakota winters. I bought my car with about 60,000 miles on her. She now has almost 180,000. She’s done about 10,000 miles a year. According to Kelley Blue Book, the average driver in the U.S. puts 12,724 miles on their vehicle each year. So, my car has more than kept up near the average in terms of production. It’s not like she’s just sat in a garage under a tarp or something.

Oh, yeah, mileage is another way to calculate the “subscription” costs of a car. Baby has only cost me 7.5 cents a mile to drive overall. For comparison’s sake, the average cost of an Uber ride per mile is $1-$2, according to Ridester. Had I bought a new car at the above-stated average price of $37,876, I’d have paid about $0.31 per mile over the same length of time. Teslas may be cheap to charge. Solar Reviews calculates a Model X would run you an eye-popping nickel per mile. But that’s after you drop an even more eye-popping $122,190 on the base model. Over 120,000 miles, that comes to almost $1.02 per mile.

Put another way, you’d need to drive that Tesla for 1.6 million miles to get to 7.5 cents a mile like my senior car. Baby wins again big time.

Now, having said all this, I realize Major League Cheapery is not the preferred route for many, as it has been for me. I’m a rare case, most likely. I am not a car guy. There are a hundred other things I’d rather buy/invest with my money than a machine that transports me to Wal-Mart for the weekly freakshow.

However, I think breaking down the cost of something into a subscription model is a great way to examine whether what you’re getting is a good deal or not for your money. What is considered a “good deal” will mostly be proportional to your income, but there’s also a fair bit of subjectivity here, too. For instance, I find most large SUVs wastes of space and fuel. But for someone who has a large family, or goes camping a lot, or really needs the extra space, it might be a good value for them. I grew up riding around in a Chevy Suburban myself as the oldest of four kids, so I get how important an approriate-sized vehicle is for a family.

What’s important is that your monthly “subscription” be proportional to your income and needs as much as necessary. If you’re paying as much for a car as a mortgage, you’re almost certainly paying far too much. This is why I compared my monthly car costs to that of my smartphone and utility bills.

For me, my car is like any other small bill. It hardly eats up a noticable percentage of my monthly budget. It’s no big deal, cost-wise. But it’s a very big deal when you consider that saving so much money has allowed me to get far closer far faster to financial independence.