You know those crazy videos where someone goes skydiving or performs parkour stunts on the edge of a skyscraper? The ones that give you sweaty palms just watching them?

That’s what it feels like reading about a middle-aged guy with a family who sank his entire fortune into a brand spanking new digital currency that just popped into existence.

Now, in retrospect, this may not seem like the absolute worst, most insane idea anyone’s every had to make a fortune. Since its inception at around $2 in 2015, Ethereum has climbed to as high as almost $4700 back in November, 2021. It currently sits at just over $2300.

But we’re talking almost ten years ago. When Bitcoin and the entire crypto market were still in its toddler years. It was the wild west.

Conway’s idea was partly inspired by Bitcoin’s shocking success in 2013, when it ran from under $100 to over $1000 in a matter of months. Could Ethereum perhaps replicate the same sort of mindboggling returns? That was the big question.

At the time, Conway was 45, “quietly desperate,” and slaving away as a corporate middle manger in San Francisco, making $150,000 a year. He was married with three kids, had about $100,000 in savings, and some built-up equity in his home. While not destitute by any means, Conway was like a lot of people willing to do anything to escape the 9–5 grind. Making matters worse (or better, depending on your POV), Conway had a somewhat addictive personality. He’d struggled with alcohol and drugs. He was even in a 12-step program.

But he was able to channel his “mania” into a new obsession — this strange new cryptocurrency. As he learned more, he became more confident that ETH could potentially replicate Bitcoin’s success from years earlier. His belief was partly due to his experience working for Macromedia in the ’90s, the company behind Flash. He was familiar with how a new tech product with the right developers can suddenly catch on and rapidly soak up market share.

Still, ETH was so new that even his friends in the San Francisco tech world didn’t believe in it.

“Most of my friends in tech — folks working at places like Google, Apple, and Uber — were dismissive of blockchain. Few of them had heard of Ethereum. When I told a buddy of mine that I was considering investing in cryptocurrency, he broke out in laughter, as if I’d admitted I was hedging my future on Smurfberries or Scooby Snacks.” (Source)

Nonetheless, in mid-2016, Conway went to his bank Wells Fargo and transferred his family’s entire life savings to the new crypto exchange Gemini (founded by the Winklevoss twins) for nearly $7,000 ETH tokens, at a price of about $14.

Then something catastrophic happened.

All of a month later an Ethereum project got hacked and Conway’s $100,000 investment sank to less than $40K. It was a harsh welcome to the world of crypto. While most people might have capitulated, the sudden reversal only cemented Conway’s belief in ETH’s potential. He doubled down. Big time. By sinking over $200,000 of home equity into the dip. Now he was all in at $300K but at an average price of about $11 a token.

As it turns out, the frightening flash crash was the pivot point. Over the course of the next year crypto saw a return of the bull market. Ethereum climbed from its bargain basement price of $8 to over $1,300.

By the time Conway cashed out in late 2017 into early 2018, his risky bet had turned into $10 million.

However, there was a huge personal toll to pay on the path to decamillionare status. Conway admits to a lot of emotional volatility, obsessively tracking ETH’s price, and late soul-searching nights worrying about his crypto account getting hacked. He was fired from his job. He even wound up in the emergency room with a “panic event.”

I find Dan Conway’s story equally thrilling and inspiring. Even somewhat relatable. I had some success with Ethereum, Bitcoin, and other cryptos myself back in 2020. It was reading stories like his that motivated me to finally step outside the comfort zone of my more conservative investing style, and take a little risk on this new asset class. I started with Bitcoin when it was under $10,000, and then Ethereum when it was sub-$500. While my returns aren’t nearly as high as Conway’s, I’ve still done okay. Time will tell whether the crypto market will undergo another face-melting run like before.

Conway is a unique personality. Very few people would be willing to go all in on something so unproven as a new crypto token like he did. Especially at 45, with three kids, a wife, and a mortgage, living in one of the most expensive areas of the country. There’s something very admirable about that. Reminscent of the Old West gold rush prospectors, or the family’s that traveled West on the Oregon trail.

However, Conway is very aware of his good luck:

“I banked everything I had on a relatively unproven technology and got out at the right time. For every story like mine, there are hundreds of others about people who lost it all. I know that could’ve easily been me.

At the same time, I’m no blackjack player. My investment wasn’t purely a blind gamble that came up aces. I was, and am, a true believer in crypto — and I had the right mix of courageousness and craziness to take a big risk.” (Source)

Since striking it rich in crypto, Conway has retired to a more normal life. He’s written a book called Confessions of a Crypto Millionaire. If you want to read more, you can also check out his first-person account of all the action in The Hustle.

Would you be willing to go all in on an investment you believe in? Was Conway crazy or ahead of the curve?

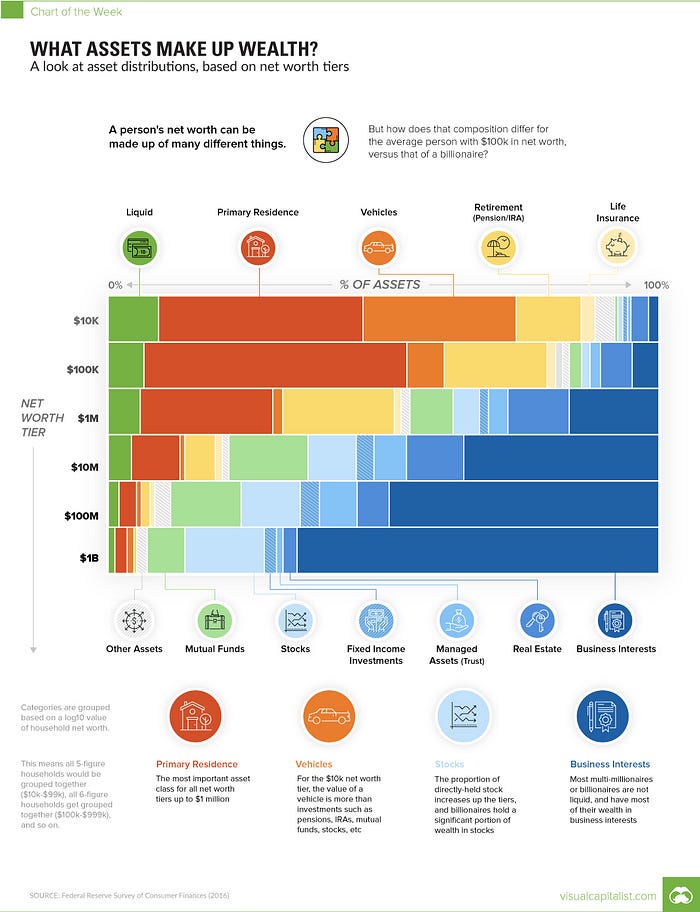

The graph comes from Visual Capitalist, a clever website that takes complex information and distills it into to easy to understand (and colorful) charts.

The chart displayed above is based on a Federal Reserve Survey of Consumer Finances from 2016, and it contains some illuminating aspects about how people in different net worth tiers manage their wealth.

Like many, I’ve always been under the impression that stocks and mutual funds are the best ways to build and maintain wealth for the average person. Over the last few years, I’ve diligently maxed out my 401(k) and IRA funds. I contribute regularly into a personal brokerage account. Even through the Covid Crash and the 2022 drawdown, I kept plugging away, dollar-cost averaging into the market like you “should.”

The returns have been solid, for sure. While I’m not close to retirement anytime soon, I’ve built up a decent net worth. I like to think I’ve “secured the bag.” Meaning that even if I never contributied another dime to my investment accounts from now until age 65, compound growth alone would get me to a comfortable retirement. And that’s NOT taking into account potential Social Security payments.

I say “potential” because who knows if Social Security will exist by then, or pay out what it’s supposed to. It’s never a good idea to bank your life on a government program, especially when the government is over 30 trillion dollars in debt.

However, the above chart has made me completely reevaluate my relationship with invesing and money in general.

For starters, the chart shows that the higher a person’s net worth the more they have invested in “business interests.” These are businesses someone owns personally. They could be anything from a franchise, a laundromat, a service company, all the way up to a controlling stake in a Fortune 500 company.

What’s surprising, however, is how little percentage-wise wealthy people are invested in stocks and mutual funds relative to their net worth. The chart combines net worths together and works out an average. So in the row where it says $10K, it’s grouping all the people with $10K through $100K together. Then in the $100K row, it’s everyone with a net worth between $100K and a million. So on and so forth.

People in the $1 million to $10 million range look to have close to 40% of their net worth in retirement accounts, stocks, and mutual funds. This makes sense give that most people in that range are retirees who spent years contributing to company 401(k) plans, pensions, and their own IRAs. About 30% of their net worth is in their primary residence.

However, going further up in net worth on the chart shows that the wealthy have increasingly less in stocks and personal homes, and vastly more locked up in their own businesses.

For those in the $10M+ group, stocks are no more than about 30% of their net worth, and their personal homes aren’t even 15%. Their wealth is mainly all in their own businesses.

This may seem obvious. But almost everywhere you turn, you only ever hear about the importance of investing in a diversified portfolio of mutual funds and ETFs.

Dave Ramsey touts mutual funds like a religion to his millions of listeners.

But are index funds and mutual funds really the best ways to build wealth?

If you were to ask most people how they think they can get rich through investing, most would probably say by getting lucky on a stock or cryptocurrency.

This is not impossible, of course. A mere $10K in Apple stock 20 years ago would be worth almost $5 million today. Buying Bitcoin or Ethereum just five years ago would have given you substantial returns.

People may remember the “meme stock” craze from just a few years ago with Gamestop and AMC. The whole internet was gripped with trying to ride the next big thing “to the moon.”

Let’s not even talk about the NFT nonsense.

Point is, everyone thinks stock investing = getting rich, except people who actually are rich. They know stocks and mutual funds won’t make you rich. They can make you financially secure. But if you want to become truly wealthy, you’re best bet is by starting your own business.

Think about it. Stock picking is unreliable unless you know what you’re doing. If you decide on the safer, diversified route of index funds, ETFs, or mutual funds, it could take decades to build anything substantial. It’s also highly unlikely you’ll break into the top 1%.

To get to $5 million, for example, you’d have to invest $18,000 a year every year for 40 years at an average annual return of 8%.

Wait, only $18,000 a year? That doesn’t sound too bad.

Well, according to the National Board of Labor Statistics as reported by USA Today, the average salary in the United States in Q4 of 2023 was less than $60,000. So, the typical person would have to stock away almost 1/3 of their income for basically their entire working life to get to that $5 million. That’s a pretty tall order considering they still have taxes and bills to pay.

—

This information may sound sobering, or even despairing. Especially to 401(k) and IRA maxers like myself, stock market junkies, or those in the FIRE (Financial Independence Retire Early) camp.

It’s important to keep some perspective. A $1 million net worth is still a lot more than most people will ever have. I’d argue you probably don’t even need half of that to retire, provided you manage your money well and are prepared to live modestly. And those are certainly attainable amounts for those who prefer the more traditional route of diversified index fund investing. Investing $3600 a year over 40 years at 8% gets you to a million.

But why cap your financial potential with just mutual funds?

What I’ve taken from this chart is that to become wealthy you’ve got to get creative and entrepreneurial. While I’m going to keep investing in stocks and my retirement accounts, of course, moving forward, I’d like to start thinking beyond them. I’m going to start allocating some of my income toward experimentation with businesses. This will prove a tough adjustment for me, as someone who’s never had his own business or been much of a risk taker. No doubt there will be some failures and surprises along the way. But I think it will be good mindset shift in the end, and hopefully a lucrative one, too.

Last year, I decided to finally purchase gold and silver bullion. Not because I thought the apocalypse was imminent. Or because I thought the economy was collapsing. Gold and silver bugs have long been lumped in with bunker-building doomsayers and economic Chicken Littles. I’m neither of those things. Even if civilization were to collapse, you wouldn’t want to be holding gold and silver anyway. In a post-apocalyptic society, things like food, water, clothing, bullets, gas, and oil represent far great currency than the yellow metal and its gray counterpart. You only need to look at places like Venezuela to see that.

No, it was curiosity and interest, and the desire to diversify my investments. I’ve been in stocks and options for years now. Two years ago, I got into cryptocurrency and DeFi. But last year, I finally made the plunge into the precious metals asset class.

Since then, I’ve accumulated what you might call a good “starter kit” of silver and gold, and the experience has been rewarding and fulfilling.

But why “invest” in gold and silver?

Firstly, it’s not an investment. It’s not even an “inflation hedge,” as gold is often touted as by the late-night infomercials. For something to truly be an inflation hedge, it should consistently outpace inflation. Gold and silver haven’t really ever done that over the last ten years. Going back over their history, there are much better asset alternatives that would have given you much higher returns. S&P 500 and NASDAQ ETFs and index funds, as well as your standard growth stocks, for example. Gold and silver on the other hand will generally just sit there collecting dust as far as the inflation-beating game goes.

Okay, so why would you put any money into them if you’re almost guaranteed to lose against inflation? Wouldn’t that money be better spent in an index or mutual fund, or something like Tesla or Bitcoin?

I think of gold and silver as a specialized savings account.

A traditional savings account offers little to no interest and may even cost you money depending on fees. If inflation continues at its current rate of about 8%, if you put $100,000 into a standard savings account, by the end of the year the purchasing power of that money is roughly equivalent to $92,000. That’s like throwing $8,000 into a bonfire. Gold and silver, however, will maintain as a store of value over the long term. Both metals have had their peaks and valleys over the last twenty years. But relative to the U.S. dollar, they’ve held strong.

They’ve also held up for almost 5,000 years of human history. One ounce of gold during Roman times bought you a nice outfit, a belt, and shoes. An ounce of gold will still buy you that now. Remember, with precious metals you have to take the long view. Don’t think in terms of years or even decades, but centuries. This is another reason I like gold. It’s “eternal.” Apple and Microsoft have delivered exponentially greater gains over the last 40 years of their existence than gold and silver have. But will those tech giants still be dominant or exist at all in another 40 years? Or eighty?

Putting your money into gold and silver is like putting it into cryostasis. You’re saving it for the future, and locking in the value of your hard-earned net worth. Even if gold and silver aren’t measured by the dollar in ten or twenty years, whatever currency they ARE measured by will likely properly match their value. This is why gold and silver are often referred to as “safe haven assets.” They have significant utility. Half of the gold in circulation is used in jewelry. The other half is used in industrial purposes and collectibles. It’s unlikely gold will lose its luster as a form of decoration in the future. And electronics will probably always have a need for gold. Silver also will maintain its industrial use into the future.

I think it’s important to own a non-liquid asset that you can’t just trade away with the swipe of a finger.

This is more of a philosophical rationale. We live in a disposable society in which so many things have become cheap, fast, and easy, like microwave dinners. Retail traders shuffle through stocks on smartphone apps like Robinhood and WeBull with the speed of a Las Vegas card dealer. Most trading on Wall Street isn’t even done manually, but with bots ruled by algorithms. I’ve traded hundreds of thousands of dollars of stocks and options myself to the point where sometimes the money doesn’t even feel real, but more like video game points. Money today, while as valuable and important to have as it has ever been, feels increasingly gaseous and fake. And not just because the Federal Reserve prints it out of thin air. But because it’s often disconnected from the hard labor, work, and risk that used to be required to possess it. For most of human history, if you wanted to make a fortune, you had to conquer someone else who had one. Or you had to be willing to face real danger, like crossing an ocean to seek trade. But capital is generally pretty easy to come by now, and this is only compounded by the ease with which it can be managed on a smartphone. A few taps on a piece of glass and you can move millions. Billions, even. It’s astounding how modern technology, while insanely convenient, has made the act of making money feel devalued and denigrated.

I like gold and silver because I like the idea of my money, my labor, and my time, being represented in something physical that’s been around for millions of years. Not just represented by a few digits on a computer screen.

Buying gold and silver can make you more responsible.

Wait, what? Precious metals can do that? Somewhat. It will certainly necessitate buying a safe for secure storage. It will literally force you to take into consideration the best way to protect your wealth. It prompts you to consider how and where you can store your precious metals. Which in turn prompts you to be more mindful of your surroundings, and your future. Even though you’d think keeping valuable pieces of metal in your home might make you worried for their security, in my experience it’s actually been the opposite. It’s a comforting feeling keeping metals under my roof. Just make sure you don’t go blabbing about your gold and silver to just anyone. And make sure you buy a good safe, particularly one that can withstand the elements, like fire and water. Most safes, as I discovered during my search, are actually ridiculously easy to break into (thanks LockPickingLawyer). But that doesn’t mean you shouldn’t buy one with some serious weight. The more precious metals you’re looking to buy, the better (and larger) your safe should be. Of course, you can always keep your metals inside a third-party vault, but that defeats the purpose (and to me, the real appeal) of owning them in the first place.

Afterall, one of the reasons Bitcoin is heralded as a valuable asset, is because you can self-custody it outside the control of any centralized entity, like a bank or government. Gold and silver have that same feature. Once that sliver of yellow or gray is dropped off at your door, or after you pick it up at a reputable dealer, it’s yours to have and to hold. Just make sure to keep a good eye on where you put it.

There’s also the diversification aspect to owning gold and silver.

When it comes to a lot of investments, people are quick to look at the ROI. The bigger the better, right? Except there’s a little thing called the risk curve. The greater the return on investment, the bigger the risk, generally speaking. Plain Jane mutual funds and bonds equal lower risk. That latest doggy-themed coin: high risk. Precious metals are closer to the safer side of the risk curve. It’s not a bad idea to own a little bit of every asset class, while focusing on the traditionally more successful and reliable ones. Stocks and real estate are always great. Crypto and Bitcoin are the future. But to me, gold and silver serve as an insurance policy. And even potentially as a “do-over fund,” if things really hit the fan. Bitcoin has the self-custody feature. But the downside there is that it’s volatile. Gold and silver tend to be pretty stable. Should you ever need to cash in your metals, there’s a good chance what you paid for them is close to what you’ll get, minus what you paid over spot.

This next reason is a little morbid, but it’s something you have to think about.

What are you going to pass down to your loved ones when you die?

Imagine being able to give them gold and silver, like you were some Medieval king (or a pirate). How cool is that? Call me a sentimentalist, but I like the idea of giving my future children and spouse something beyond just paper assets. Sure, real estate is fine, but it’s hard to split a house. A business is good, but your heirs may not want to or be able to continue running it. Gold coins and silver bars are easily divisible, and simple to trade-in for cash value.

There’s another smaller and sillier reason that motivates me to buy gold and silver.

I grew up loving Scrooge McDuck, from the Duck Tales cartoon. While I never thought I’d ever have a money bin filled with gold coins (and a Number One Dime) like he did, I always envisioned being able to have at least my own collection of coins.

A few things to consider before getting into precious metals.

Make sure you buy from a reputable dealer.

I use JM Bullion, which is a pretty well-established company. I’ve never had an issue with any deliveries. They have three pricing tiers depending on the method you use to pay. Electronic check is generally the cheaper option, but you can also use a debit card, or cryptocurrency. Be prepared to wait about two weeks if you use the e-check method. It’s worth the wait for the discount, though. Afterall, it’s not like gold or silver have expiration dates. A good dealer should ship your delivery discreetly, but you should make sure that your package requires a signature. If you live in an apartment building with a management office, try to have UPS deliver there, if you can’t have them deliver straight to your door. If you are shipping to your own house, either make a signature required, or make sure you or someone you trust is there for when the package is scheduled to arrive.

Get a good safe.

Or at least one that will withstand the elements, mainly fire and water. You don’t have to go all out and spend thousands, necessarily. But you want one that’s heavy enough to prevent someone from just easily walking off with it. Your safe’s size and cost should be proportional to your expected holdings. For a first-time buyer, a simple Sentry safe with a combo lock might be sufficient. It’s what I use myself. More experienced or higher net worth buyers may want something larger. You may also want to even look into keeping your metals in a vault with a private company. Or even in a safe deposit box. Whatever works for you.

Mind the over spot fees.

This is really important to consider, and it’s even something that puts some people off from buying precious metals in the first place. When a dealer like JM Bullion sells you gold, they add an over spot fee to the trading value of the gold item. So, if gold is currently trading at $2,000 an ounce in the market (AKA the “spot price”), JM Bullion might sell you a one-ounce gold American Eagle for $2,100, which would constitute a $100 over spot fee. Dealers have to collect a profit to stay in business, obviously. But depending on the over spot cost relative to the market price of the metal you’re buying, it can make a purchase more expensive than you might expect. A rule of thumb is that generally the smaller weight a metal is, the greater the proportion in over spot fee will be.

Silver has a much higher over spot cost than gold. A one-ounce American Eagle silver coin currently retails for $38 or more on JM Bullion, while the price of silver is at around $25. That’s almost a 50% mark-up! Yeah, silver coins are generally not really worth it, especially during periods of high demand like right now. It gets worse when you consider that if you were to sell your silver back to JM Bullion (or anyone else), you’ll likely only get spot value ($25 an ounce), NOT the over spot cost you initially paid. So, if you’re buying silver coins, you’re in the hole from the beginning. Not the best way to start a new relationship with a new asset. But again, this is why gold and silver are NOT true investments, but specialized savings accounts.

Remember, you’re also guaranteed to lose purchasing power if you hold your money in a traditional savings account in a low-rate environment (like today). But the value of keeping reserves liquid for an emergency, or saving for an upcoming purchase like a down payment on a house, is worth more than the risk of your money gradually losing out to inflation.

Some of my ten-ounce silver bars

To help mitigate the over spot fee for silver, I purchase ten-ounce silver bars, which in calmer market periods often only retail for about $3 or so over spot per ounce. The larger size you buy, the lower the over spot fee, generally speaking. JM Bullion also offers a discount on over spot if you buy in bulk. Though I don’t think I’d ever buy a kilo or 100 oz. bar of silver due to weight and storage issues.

I also don’t buy silver collectibles, such as silver bullets or figurines, or “junk silver,” aka old coins like quarters that were minted with real silver. I’ve found the over spot fees there especially egregious, to say nothing of the questionable “value” in those silver items. Many people buy gold and silver for emotional reasons over purely logical reasons. Metals are assets that make people “feel secure,” especially during turbulent times in the stock market, or during violent geopolitical affairs. This is why many precious metals dealers like to play on people’s fears in their marketing efforts. Dealers like JM Bullion market a variety of gold and silver products on their sites. JM even has a whole line of Disney-themed coins. If you’re into those sorts of products, fine. But collectibles need to be evaluated differently. You’ll almost certainly overpay not just on over spot fees, but mark-up, as well. For me, I stick solely with gold and silver bullion, and I don’t collect or wear jewelry.

As for things like commemorative coins, rare coins, or “proof” coins and such, you’ll also pay substantially higher premiums. The value of those sorts of coins is more in their scarcity and demand in collector circles, than in just their gold or silver content. They are better used as gifts than as “stores of value.” Last year I bought sealed American Silver Eagle coins for my newborn niece and nephew, for instance.

If you’re really serious about acquiring a lot of bullion, gold is going to be your most cost and storage-efficient option. Silver is nice and cheap to start out with. But its high over spot fees don’t make it worthwhile for the average person. To say nothing of the impracticality of trying to store large amounts of the metal. You can easily stick $10,000 in gold coins in your pocket. You’d need a shoebox to carry $10,000 worth of silver, and it’d be heavy to lug around.

For gold, I’ve found that you want to stick with at least one ounce or higher to keep those over spot fees low. Anything less than an ounce, and you’re overpaying substantially. For example, a quarter ounce American Eagle gold coin on JM Bullion currently goes for about $629, with gold at $1941. That means you’re paying almost $144 over spot, or almost 23%. Whereas if you buy the one-ounce American Eagle, it’ll cost you an extra $130, which represents a more tolerable 6.6% over spot cost. The coin posted at the top of this article is the British Britannia. I bought this coin not just for its beauty and its sensational design, but also because it offered the lowest over spot fee for a gold coin. As of now, the over spot cost is only $84, making it one of the best deals currently on JM Bullion.

The absolute cheapest way to buy gold with the lowest spot price is to buy the prepackaged bars in sealed plastic, either the one ounce or the ten-ounce kind. However, I really prefer the coins. The slightly higher over spot fee is negligible compared to the savings you get with the bars. And they just look cooler, too.

Another thing to consider is the purity of the gold you are buying.

American Eagles, for example, are .9167 purity. The remaining .0833 is a mixture of silver and copper to help protect the finish and make the coin tougher and harder to scratch (gold is a soft metal, remember). Even though American Eagles are among the most popular gold coins on the market, if you’re a purist like me, you may prefer as much gold as possible. Since American Eagles are only about 90% gold, while still having a higher over spot fee, I don’t find them to be a good deal. The British Brittanias, on the other hand, are .9999 purity, not to mention have a sharper design. And since I keep mine locked in a plastic holder anyway, I’m not concerned with it getting scratched. So, it eliminates the mixed-metal toughness “advantage” American Eagles have.

Most silver bullion is going to be .9999, so there are generally no purity issues to be concerned with there.

Lastly, you’ll want to carefully consider portfolio allocation.

This is going to be different for every individual. For me, I probably wouldn’t keep more than one or two percent of your net worth in precious metals. Remember, you are essentially “freezing” any money you put into metals. Money that won’t be potentially collecting dividends or increasing in value like it would in a good growth stock, ETF, or index fund. Money you can’t use to save toward a down payment on an investment property, or a small business. It’s also not money you can easily and quickly make liquid for emergencies. And, of course, you don’t want to have more than you can reasonably hold and secure in a good safe. It’s really not necessary to go heavy into precious metals.

A final word of caution. It’s very easy to get bit by the gold bug. Gold’s a metal that has attracted mankind for over 5,000 years, after all. It’s tempting to start collecting a lot more after you get your first shiny new coin or bar. But try to keep it in moderation.

I’ll leave you with a few interesting and fun facts about gold.

That’s a fascinating factoid, to be sure. But it got me thinking. How would one measure all of the gold in the form of Mr. T’s? Mr. T., as in the ‘80s pop icon famous for wearing myriad gold chains. Mr. T as in “I pity the fool.”

Mr. T is reputed to have worn approximately 100 ounces of gold, which incidentally would be valued at nearly $200,000 at the current spot price. That means you would need about 86,068,467 clones of Mr. T, all fully decked out in their gold chains, bracelets, and rings, to carry all of the world’s currently known gold reserves (including already mined gold and some discovered, but remaining in the earth). That’s almost the whole population of Germany. That’s a lot of Mr. T’s, and a lot of gold chains.

But you don’t have to be like B.A. Baracus, wearing enough metal around your neck to buy a Ferrari. You can start with a starter kit. A few “stacker bars” of silver. A gold coin or two. Maybe even diversifying further into alternative metals like platinum and palladium, if that’s your thing. Gradually scaling upward as your net worth climbs over time. Whatever you choose to buy, you’ll find precious metals collecting rewarding and fun.