A few common sense tips to avoid some common pitfalls.

I’m constantly seeing all kinds of articles about side hustles and other ways to make money and become wealthy.

While these are helpful, I’ve found that building your net worth is less about what you do and more about what you don’t do. Unfortunately, nobody hands you a guide called “How Not To Fuck Up” when you turn 18, that shows you the many spring-loaded bear traps laying about out there. In fact, it seems people are more apt to let you walk right into one and snap your leg off.

Nobody was there to tell me anything. So some of these pitfalls are ones I learned myself, the hard way. Others I was fortunate to avoid on my own.

Finish High School And Keep Your Fucking Legs Closed (meaning don’t have kids) Until You’re Married.

I combined these two tips because they are common refrains from Dave Ramsey. It really is that simple. If you do these two things, you are virtually guaranteed NOT to end up in poverty. Do one of them, and your chances of one day becoming financially successful are very low. Do both and it’s almost impossible. The welfare register, the ghettos, and the trailer parks are filled with people who did both or either. I’ve met many single moms in my life who were not married before having a kid, and virtually all of them were in the poorhouse and on government assistance. I’ve met guys who had kids when they were super young, and nearly all of them were broke.

Guys are less threatened by this pitfall because young children are not physically dependent on us to live, obviously. We’re also expected to work regardless of our ejaculative accomplishments, too. But for women, this is a crucial, even life critical step. Having a baby with some lowlife dickbag loser who runs off, then not having the legal and financial support that a committed marriage provides, can seriously fuck you and the kid up for life.

Even in a good marriage having kids is tough. And yes, people divorce and go through hell. But trying to raise a kid while dealing with baby daddy or baby momma drama is a complete fucking nightmare and almost impossible to work through. Yet millions stumble into this pitfall every year. It may be funny to watch child support fights or paternity drama on Judge Judy or Maury Povich, but in real life this shit is tragic and often forms the basis for why our society is so fucked up. So, to be clear:

Keep it in you pants if you want to keep money in your wallet!

Don’t Take Out Student Loans For Stupid Bullshit Degrees. Let Me Repeat That. Don’t Take Out Student Loans For Stupid Bullshit Degrees.

This is a BIG one. And it hits home because I fell into this pitfall myself, and it seriously screwed me up for years. I mean, I would be a completely different person today had I not borrowed money for college. I would not be living where I am. I would not have gone through hell as a result. I might even be in a better place. While I’ve since cleaned up the disaster I made for myself and am doing quite well now, I lost YEARS and therefore OPPORTUNITIES because I needlessly saddled myself with student loan debt.

Here’s the deal. For years, only the wealthy earned liberal arts college degrees for a “well-rounded education.” Then the banks, working with the government, came along and convinced everyone else they could and should too, even if that meant taking out vast sums of money. Now you have millions of college graduates stuck with trillions in student loan debts they can’t discharge through bankruptcy, while having no real employment prospects, and therefore no income. You have young people graduating with $100k+ in debt for fucking useless art degrees.

There’s a reason only the wealthy used to do this. Because they knew they had a job at daddy’s company when they graduated. They knew they’d end up on their feet. As harsh as this is to say, if you’re middle-class or lower, you’re almost certainly wasting your time and money by doing the same thing as the rich. Sorry, no, you don’t need a “well-rounded education.” You’ve been duped by banks and the government. What you need is fucking money. You’re not sophisticated and elite because you learned about the French Revolution and fill-in-the-blank-philosopher’s-name, you’re poor and broke. Unless your degree leads to a real career with real prospects and real money, do not waste one goddamn second on it.

I look back at my stupid idiot self. I took out over $25,000 in loans for a degree in political science from a private college that I had absolutely no business attending. I hated it there, too. Most of the students were, unsurprisingly, trust fund kids, or at least had big help from mommy and daddy toward paying tuition. I did not fit into the scene whatsoever being a broke mixed-race kid from the other side of the tracks. I left after one year without a degree. Obviously, I had no help myself other than what I could scrounge up through financial aid. I’m not even proud of the fact that I qualified to get in to this school. I’m ashamed, because going there left me in debt with no way to repay. I wound up working in a fucking department store afterward before getting back into the printing trade.

To say that student loan debt ruined my life would be an understatement. Robbing a bank would have fucked me up less. At least then I’d have a cool story and some prison tats.

Look, I get it. The allure of an “elite” institution is hard to overcome. Everyone wants the prestige of a four-year degree from a “top” college or university. But the reality is, especially in this day and age, it’s not necessary. And if you’re poor, it might even be financial suicide. If you want a “well-rounded education,” go to the library or watch YouTube. They’re both free.

The delusion over degrees is un-freaking-real. I could go on for hours. One time I met an obese broke single woman in her mid-20s who was a few months pregnant. She was convinced she was still going to get into a prestigious law school in New York City and become a lawyer and fight for “women’s rights” or some bullshit. I asked how she planned to do this with an infant, no money, while living in one of the most expensive places in the world, all to chase a profession in what was certainly low-paying non-profit work, to which I received only a derisive snort and nostril flaring in response. As though I were a complete idiot for even asking. I never saw this lady again, but I’d be willing to bet she ain’t hobnobbing with high-powered feminist do-gooders in Manhattan.

Drive A Shit Box You Paid In Cash For Because You Don’t Need A Luxury Vehicle To Pick Up Hungry Man Microwave Dinners At The Grocery Story.

I’ve written previously about my “senior vehicle” and how it only costs me $64 a month to drive.

I drive a 2006 Saturn Ion with over 180,000 miles despite having an above average networth for my age, and more than enough to pay for a premium new car in cash. I fucking love my “shit box.” At this point, I’m planning on keeping it and driving it for as long as possible, and giving it a Viking funeral for whenever that time comes. It’s a “grocery getter” at this point. It used to drive me back and forth between Philadelphia and New Jersey. Nowadays I don’t drive it more than 120 miles at a time. If I need to go on a road trip I rent a car or fly. If my life situation were to change and require me to upgrade vehicles, I’d still get something cheap and used and do the same damn thing that I’ve done with this car.

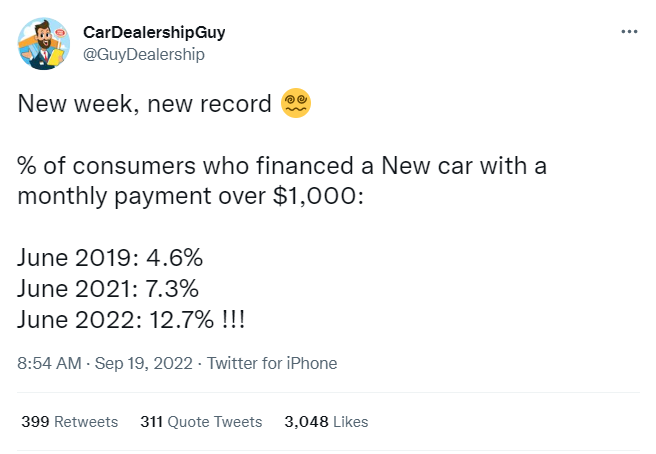

My “senior vehicle” only costs me $25 a month to insure, and very little to maintain. Because of the substantial savings I’ve made over the years, I’ve been able to put way more into my investment accounts. If I were instead one of those clowns who feels the need for a new shiny set of wheels just to drive to my crappy cubicle job, I’d not have been able to max out my 401k, my IRA, and build up a solid net worth that has put me on the path to financial independence and early retirement. The average car payment nowadays is around $700 a month, which means many people pay WAY more than that. That’s just the financing payments. There’s insurance and maintenance on top of that. You have people literally pissing away millions in potential compound gains because they need to sit in a metal box with a name brand logo on it. Absolutely ridiculous.

Once again, for many years, only the wealthy bought premium vehicles because only they could afford them. Then along came “easy” financing schemes and loose lending standards by the banks. Now everyone can “afford” to buy BMWs and Mercedes and SUVs that cost a gold brick to fill up at the gas station. This is why you see hot rods parked in the ghetto, and those giant monster “America-fuck-yeah!” trucks parked in the sticks. Isn’t “equality” great? Well, it’s not really equality, because those people still can’t afford those vehicles. They can only (barely) afford the $1000 monthly payments. At least until they lose their job. Then it’s the repo man laughing all the way to the bank. And the dealership, too, which just turns around and sells the car to another sucker who needs to compensate for his inadequacies by overpaying for a pile of plastic and sheet metal that can move 70 M.P.H.

All these tips basically boil down to “Don’t buy shit you can’t afford.” Which seems easy. But so much of money management has nothing to do with math, but emotion. People attach emotional value to things like college degrees or vehicles that they really don’t need, that they don’t realize will screw them for years to come. People get irresponsibly caught up in the passions of a relationship and wind up trapped with offspring they are not prepared for or capable of properly taking care of.

People have gross misunderstandings when it comes to money. Many think making big money is all about some big score or windfall. Winning the lottery. Making out on some stock or cryptocurrency. While a lucky few will hit those jackpots, for the most part, building wealth is a largely a “brick by brick” deal. It’s a stifling boring process, actually. People overcomplicate it. But it’s less about doing a bunch of things right, and more about simply not colossally fucking up with a few wrong decisions that are actually quite easy to control.